**Breaking News: IMF Debt Crisis Looms as Countries Face Mounting Obligations**

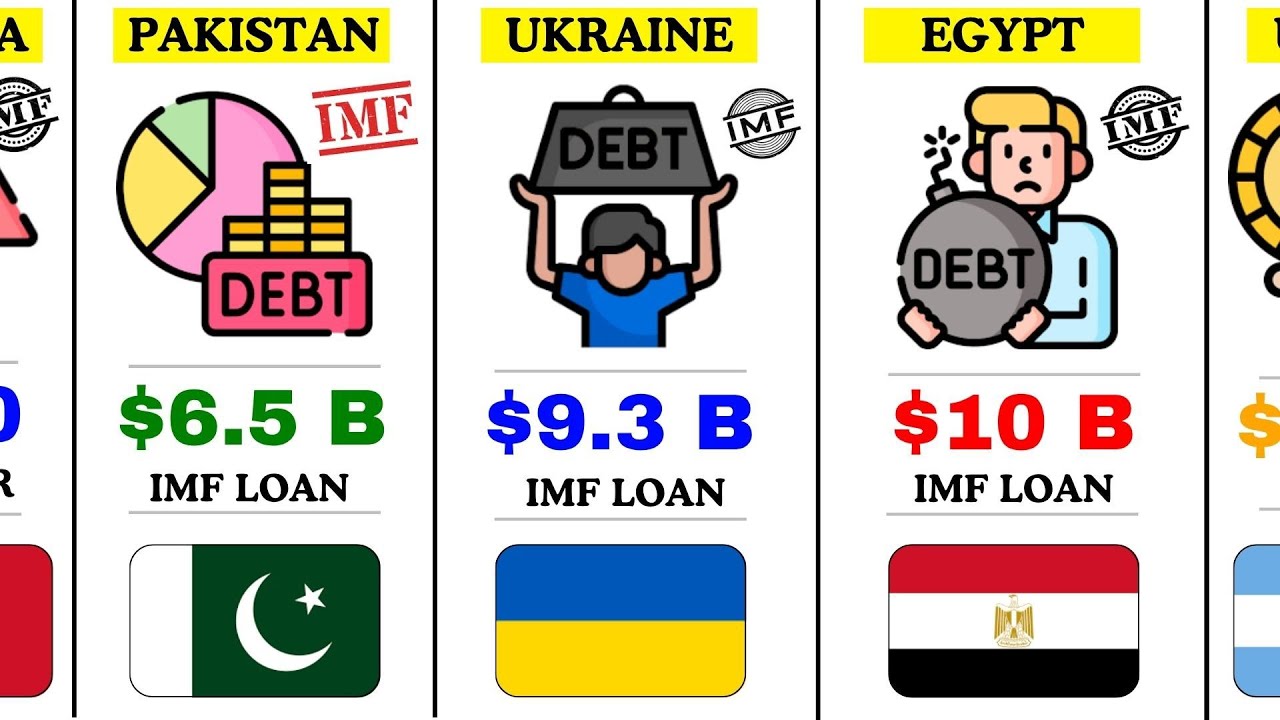

In an alarming revelation, the International Monetary Fund (IMF) has disclosed staggering debts owed by numerous countries, raising urgent concerns about global economic stability. As of 2025, nations are grappling with unprecedented loan amounts, with Argentina leading the charge at a staggering $30.9 billion, primarily aimed at economic stabilization amidst turmoil.

The crisis doesn’t end there. Egypt is burdened with $10.8 billion, desperately trying to combat rampant inflation. Ukraine, still reeling from wartime devastation, owes $9 billion for essential recovery efforts. Pakistan finds itself in dire straits with $6.5 billion in loans, as it faces a severe economic crisis.

Countries across the globe are feeling the strain. South Africa’s $1.9 billion debt highlights the urgent need for economic stimulus and recovery, while Colombia’s $3.2 billion loan aims to tackle inflation and labor reforms. Meanwhile, Kenya’s $2.5 billion obligation underscores the precarious nature of its economic stability.

The situation is dire for smaller nations too. Liberia, Haiti, and Namibia are among those struggling with debts of $162 million, $184 million, and $191 million respectively, as they seek international support to stabilize their fragile economies. The IMF’s role in these countries’ recoveries is vital, but the mounting obligations raise questions about long-term sustainability.

As the world watches, the implications of these debts could lead to a ripple effect, impacting global markets and economies. The urgency for reform and recovery has never been more pronounced. Countries must navigate these treacherous waters carefully, or risk plunging into deeper financial crises that could affect millions. The clock is ticking, and the global economic landscape hangs in the balance. Stay tuned for further updates as this story develops.